Mortgage Denial Data Reveals How to Boost Your Approval Odds

Getting approved for a mortgage is never easy. Even with great credit and a big down payment, the process can be cumbersome. In 2020, the process has become even more difficult.

Lenders have tightened standards in response to the economic uncertainty during the coronavirus pandemic. Borrowers, hoping to buy a home while interest rates are super low, are finding it more difficult to get approved.

Mortgage applications may be denied for several reasons — a down payment that’s too small or a credit history that’s too short or damaged, for example. And while more borrowers may face denials in 2020, those reasons are the same year after year.

Examining 460,000 denied mortgage applications from 2019 paints a picture of the hurdles borrowers face and suggests how they can best prepare for the application process.

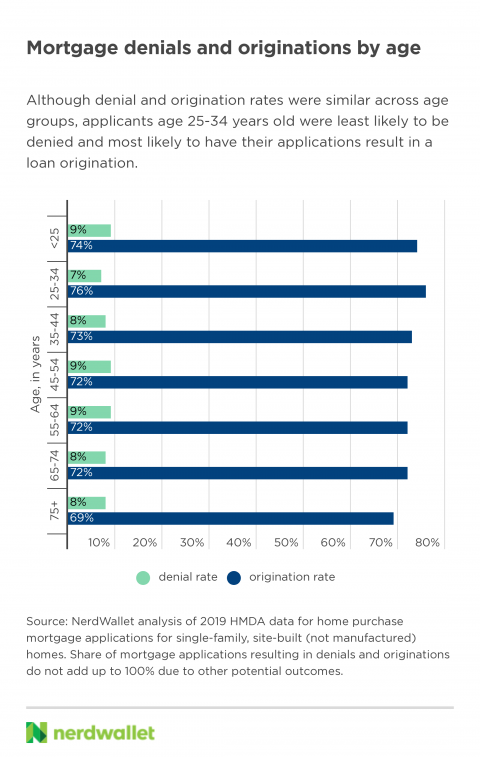

Denial rates steady across age groups and states

In 2019, about 460,000 home purchase mortgage applications — or 8% of them — for site-built (not manufactured) single family homes were denied, according to data that lenders submitted to the federal government under the Home Mortgage Disclosure Act.

The denial rate among applicant age groups was fairly similar, ranging from 7% to 9%. Applicants 25 to 34 years old were the least likely to be denied; 7% of their applications were turned down. They were also the age group most likely to have their applications result in a loan origination: 76%, compared with 69% to 74% for other age groups.

This could be due to any number of factors: These younger adults perhaps haven’t amassed the overall debt of older adults, they may be applying for first-time home buyer loans with more lenient standards, or they could be borrowing less because they are shopping for a starter home.

Denials by state ranged from 5% to 10%. Two states, Idaho and Minnesota, had the lowest denial rates (5%), while applicants saw 10% of home purchase mortgages denied in three states — West Virginia, Mississippi and Florida.

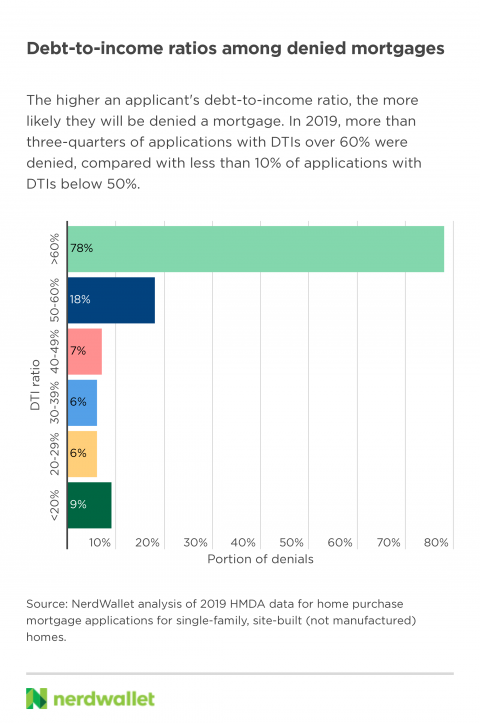

Debt-to-income ratio tops denial reasons

The top three reasons for denied applications were: debt-to-income ratio, cited in 35%; credit history (22%); and collateral, or loan-to-value ratio (18%). Other reasons were cited in fewer than 15% of denials each, including incomplete applications, insufficient cash, unverifiable information and employment history.

Debt-to-income ratio is a way for lenders to look at an applicant’s total monthly debt obligations compared with how much money they make. Lenders have different debt-to-income ratio requirements, but a DTI under 20% is generally considered low, whereas 43% is typically the highest lenders will accept for qualified mortgages, or those that require the lender to take steps to ensure you’ll be able to pay the loan off.

The risk of a denial increases significantly when an applicant’s DTI reaches 50 and above. In fact, 78% of applications with DTIs over 60% were denied in 2019.

Getting an approval: Improving your odds

Lenders take a number of factors into account when determining your ability to repay a loan (hence the lengthy application process). But taking the following steps can help you avoid being among the denial statistics.

1. Keep overall debt low.

The data indicates a DTI below 50% is far less likely to be denied, and the lower the better. A debt-to-income calculator can help you determine where you are right now, taking into account monthly debt payments such as rent, student loans, car payments and credit cards, and weighing them against your gross income. Improve your DTI ratio by paying down debt or increasing your income.

2. Build and maintain healthy credit.

In a normal year, you don’t need perfect credit to qualify for a mortgage, but the higher your credit score, the more likely your mortgage will be approved in 2020. Aiming for 700 — a bare minimum level for approvals announced by JP Morgan Chase this spring — will help you qualify for the best rates, but if that’s out of reach, get as close as you can. Some lenders and loan types — such as FHA loans and first-time home buyer programs — allow for greater flexibility. Track your credit score and take steps to build your credit, such as: keeping your balances low, paying your bills on time each month and regularly reviewing your credit report for errors.

3. Save up a bigger down payment.

The loan-to-value ratio (or collateral) on your application compares how much you’re borrowing with the value of the home. Lenders like to see low LTV ratios as they want to know their investment is protected if you’re unable to make your mortgage payments at a future date. Most mortgages with an LTV above 80% require private mortgage insurance (an additional sum tacked onto your monthly payment) to protect their interests. The larger your down payment, the lower your LTV. An LTV calculator can quickly show how your expected down payment and home price measure up.

Analysis methodology and additional graphics available within the original article, published at NerdWallet.

The article Mortgage Denial Data Reveals How to Boost Your Approval Odds originally appeared on NerdWallet.